Reverse mortgages are very popular here in Florida. Many retired people and senior citizens have them. Lots of banks like them, too.

Lenders are actively marketing for reverse mortgage business here. Maybe you’ve seen one of the various TV celebrities promoting reverse mortgages as a smart way to boost finances in your retirement years. Well, be careful, Floridians.

Growing Number of Wrongful Foreclosures on Reverse Mortgages

Florida is one of the top three states in the country where wrongful reverse mortgage foreclosures are being reported to the federal Consumer Financial Protection Bureau. According to a report by the CFPB, more and more wrongful foreclosures are being instituted by lenders against home owners with reverse mortgages.

This is a growing problem. Years ago, the CFPB issued another report warning that the agency was receiving more and more consumer complaints about reverse mortgages and lenders not doing the right thing.

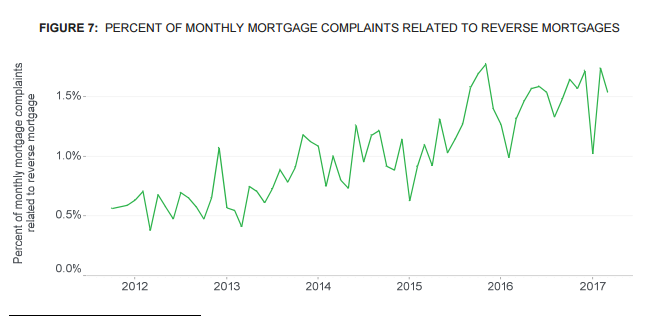

Today, “servicing problems with reverse mortgages” are one of the major complaints filed with the CFPB by consumers over the age of 62 (the minimum age to get a reverse mortgage as a general rule).

Wrongful foreclosures are being filed as a result.

Federal agency reports escalating number of Reverse Mortgage complaints: CFPB Report

What is a Reverse Mortgage?

Almost all Florida reverse mortgages are federally insured by the Federal Housing Administration as Home Equity Conversion Mortgages (“HECMs”). To get them, you have to be at least 62 years old and a home owner.

The reverse mortgage is not like a standard mortgage, where the bank is loaning money to buy the home and expects to get a monthly mortgage payment from its borrower.

Here, the bank sends monthly payments to the homeowner. How much the home owner gets as a monthly payment depends upon the equity they have built up in their home.

It’s still a loan, of course. But the homeowner doesn’t have to pay back this loan until they move out of their home or until they pass away. The payments arrive every month under the terms of the loan.

That’s right: the bank pays the borrower a set amount each month.

Here in Florida, HECMs are very popular. Seniors and retirees find that the reverse mortgage monthly payments help them to make ends meet. This can be very important to those on a limited retirement income or Social Security. And that is the big selling point for banks marketing these reverse mortgages to potential customers.

Default on a Florida Reverse Mortgage

There’s no foreclosure risk involved at first, of course. And there may never be a problem as long as the lender doesn’t claim there has been a default on the loan and tries to claim that the entire amount is now due and payable (“accelerates” the loan).

The lender has to notify the borrower of a default. Then the homeowner becomes vulnerable to foreclosure just like any other mortgage. After there has been a notice of default on the loan, the next step for the bank is to file a foreclosure lawsuit.

So what is a default on a reverse mortgage? What makes the homeowner vulnerable to a bank’s foreclosure lawsuit?

Defaulting on a reverse mortgage can happen in several ways. If the terms of the reverse mortgage are not met or the loan is not paid off as stated in the mortgage documents, then the lender may file a foreclosure action.

This can happen when:

Homeowner Fails to Keep Up the Property

When the bank loans money against the residential property in a reverse mortgage it views the home or condo as its protection against a loss. Not keeping up the property in repairs and maintenance means that the property may lose value permanently. This can be viewed as a default on the reverse mortgage by the bank.

If the bank discovers that the property is not being maintained according to the bank’s standards, then it may opt to try and take ownership of the property.

The bank takes ownership of the home or condo through a foreclosure action. From the bank’s viewpoint, it will foreclose in order to protect its investment – which is the land and its improvements.

Homeowner Moves Out of the Home or Condo

One of the conditions of a reverse mortgage is that the homeowner actually lives in the home or condo. Florida reverse mortgages are not offered on investment property like rentals.

Often, these moves aren’t voluntary. The homeowner may need to move into a nursing home or care facility for health reasons.

That won’t matter to the bank. There is usually a grace period within the documentation (e.g., twelve months). If the homeowner has not returned to live in the home at the end of the grace period, then the bank will see this as a default and may begin foreclosure proceedings.

Homeowner Rents the Home or Condo

Some lenders insist that the homeowner remain in the condo even if he can find a reliable tenant to live in the property. Renting out the property may be seen as a default by the bank and it may start foreclosure proceedings.

Homeowner Sells the Home or Condo

If the home or condo is sold, then the bank will expect to be paid in full on the reverse mortgage. It will also have a say in how much the property should sell for, usually insisting upon a sales price of 95%+ of the appraisal.

If the bank is not fully paid off after the sale or if the sale does not comply with the conditions set forth in the reverse mortgage documentation, then the lender can consider this as a default and try and take ownership of the home or condo through a foreclosure.

Homeowner Fails to Pay Property Taxes or Insurance Premiums

The lender will demand that the property taxes be paid on time. Any failure to pay taxes on the home or condo can result in a reverse mortgage foreclosure. The same is true for the failure to timely pay the homeowners’ insurance premiums.

Death of the Homeowner

When the homeowner passes away, the property immediately becomes a part of his or her estate. The Personal Representative must deal with the lender on the reverse mortgage.

Here, the bank may want to foreclose viewing the death as a default under the terms of the reverse mortgage. The Personal Representative must deal with the lender and protect the interests of the surviving spouse as well as the heirs and beneficiaries. This may mean selling the home or condo in order to cover the reverse mortgage and block the foreclosure.

Wrongful Foreclosure: Problem of the Non-Borrowing Spouse

For some Floridians, there may be an issue with the lender of a reverse mortgage if the homeowner passes away and the surviving spouse is not a co-borrower. Both federal and state law (and case precedent) exists to help these widows and widowers stay in their home despite a lender claiming default on a reverse mortgage based upon the death of the borrower.

However, surviving spouses may need to fight with the reverse mortgage lender here and assert their legal rights. The bank will be looking to protect its assets and it may try and file a foreclosure action summarily after the death of its borrower.

This may be a wrongful foreclosure action but the widow or widower will need to defend against it. If they do nothing, then the bank can get a foreclosure judgment from the court.

Wrongful Foreclosure: Escrow Demands for Insurance and Tax Payments

Many reverse mortgages today come with offers to set up escrow accounts for the payment of property taxes and homeowner’s insurance premiums. These are similar to the same arrangements offered in conventional mortgages.

However, for some homeowners there have been problems with these escrow accounts. They may have received demands for payment even though the homeowner assumes that the payments will be a part of the reverse mortgage loan.

If the homeowner is considered behind in their payment of taxes or insurance, the FHA allows them two years to become current before the bank can consider a foreclosure lawsuit. Filing before that deadline can be a wrongful foreclosure. So can any foreclosure where the insurance and tax payments were paid, or made current, or where to be paid by the lender out of the reverse mortgage loan.

Wrongful Foreclosure: What the Borrower Owes the Bank

Eventually, the reverse mortgage will become due and payable for whatever reason. However, how much the bank is due may be a subject of controversy.

As a general rule, the lender is owed only the amount of money that has been paid out to the borrower under the reverse mortgage as well as any fees and interest agreed upon under the terms of the loan.

If the amount owed the bank is not paid, then the bank can file a foreclosure lawsuit. However, this will be a wrongful foreclosure if the bank is seeking money that is not due to it.

One key issue here may be the appraised value of the home. If the home is sold to pay off the reverse mortgage, the bank may demand that it be sold for at least 95% of the appraised value.

But what if there is an improper appraisal? The appraisal alone may generate a wrongful foreclosure controversy.

Defending Against a Wrongful Foreclosure in Florida

If you are struggling with demands from a lender regarding your reverse mortgage, or you suspect that you may be, or have been, a victim of a wrongful foreclosure of a reverse mortgage, then it’s important that you know your legal rights under state and federal law.

Seeking out guidance from an experienced Florida foreclosure defense lawyer may be extremely helpful to you. Foreclosure may be avoided or reversed.

Many South Florida real estate lawyers, like Larry Tolchinsky, offer free initial consultations. Please feel free to give us a call.

For more, see:

- Did Your Foreclosure Violate the Law? Are You a Victim of Wrongful Foreclosure?

- Feds Awaken to Widespread Appraisal Fraud as FDIC Sues, Alleges Florida Appraiser LPS Appraisals Wrongfully Inflated Values.

If you found this information helpful, please share this article and bookmark it for your future reference.